WASHINGTON — Americans are familiar with the impact of higher interest rates, which are making it more expensive to carry credit card debt or buy homes and cars. But the federal government is also getting walloped: Spending on interest on U.S. debt is now the fastest growing part of the budget, and even projected to overtake national spending on defense this year.

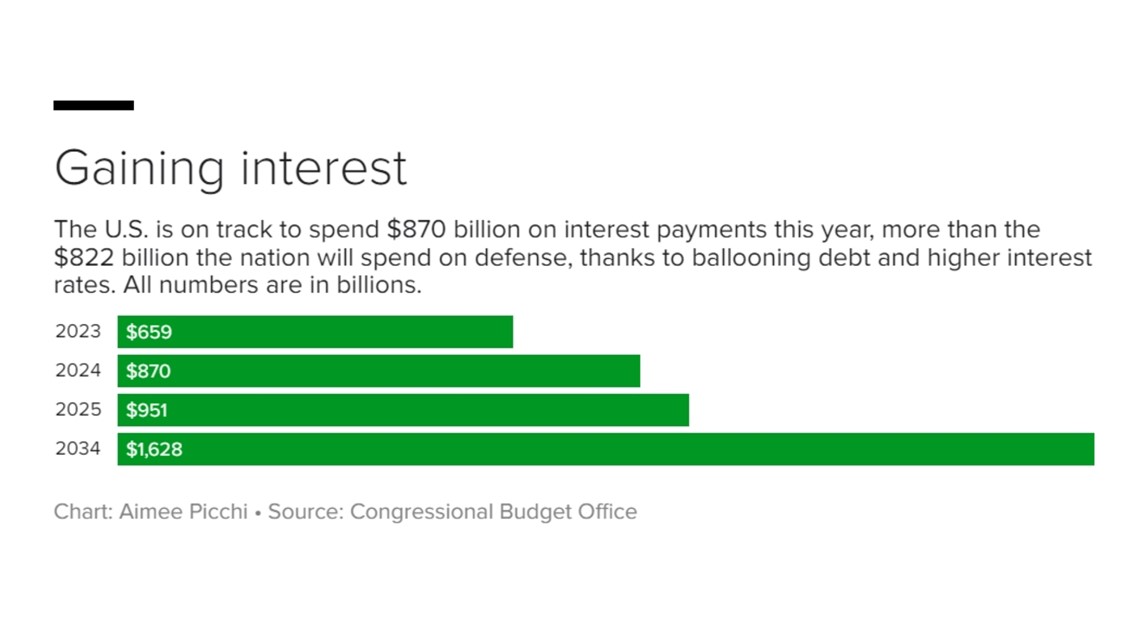

Federal spending on interest payments is forecast to hit $870 billion this year — exceeding the $822 billion that the nation will spend on defense in 2024, according to a recent analysis by the Congressional Budget Office. This year's outlay for interest payments represents a 32% increase from last year's $659 billion in interest expense.

To be sure, higher interest rates aren't the only factor raising the cost of servicing the country's debt. Over the last decade, the U.S. has almost doubled its outstanding debt, which surged to $33 trillion last year from $17 trillion in 2014, according to Treasury data.

Why interest payments have soared

The nation's ballooning debt stems chiefly from tax cuts enacted by former President Donald Trump in 2017, as well as the surge in federal aid to keep the economy afloat during the pandemic (assistance authorized by both Trump and President Joe Biden). On top of that, with the Federal Reserve turning to its most effective anti-inflation tool — higher interest rates — the U.S. is paying more for its growing pile of debt.

That's steering the U.S. into uncharted territory, according to some policy experts. The problem, they say, is that the nation's mounting debt and interest payments could eventually squeeze federal spending, making it harder to fund core programs like Social Security or to invest in initiatives that drive economic growth, such as infrastructure or education.

"Interest is projected this year to be the second-largest federal program — it means your tax dollars are going to interest instead of going to everything else," said Marc Goldwein, senior policy director at the Committee for a Responsible Federal Budget, a bipartisan think tank.

He added, "As far as I know, interest has never been larger than the defense budget."

Last year, U.S. interest payments on its debt amounted to 2.4% of GDP, and the CBO projects that will increase to 3.9% by 2034.

While that might sound dire, it's not quite right to directly compare spending on programs like Social Security or defense to interest payments, noted Bobby Kogan, senior director of federal budget policy at the Center for American Progress.

For one, interest payments are tied to financing for approved spending — in other words, the money reflects lawmakers' earlier decisions to avoid tax hikes or slash key government programs.

"A lot of folks tend to say interest is a waste of money, and that's not true," Kogan told CBS MoneyWatch. "The decision to have interest payments happened because we decided not to do tax increases or spending cuts."

Second, spending more on interest doesn't equate with cuts in programs. "It's not true that if interest is higher it's impossible to spend a dollar more on nutrition assistance," he said. "The idea that this interest is crowding out other government spending isn't mechanically definitively true in any sense."

$37,100 per person

Another key point to consider is that the nation's fiscal outlook is now in better shape than the CBO had projected it to be a year ago. That's largely due to stronger-than-expected economic growth as the U.S. recovered from the pandemic, according to senior Biden administration officials who spoke with CBS MoneyWatch.

For instance, the government's 2024 budget shortfall will be $63 billion smaller than the CBO projected almost a year ago. Meanwhile, the cumulative federal deficit over the next decade is on track to be $1.4 trillion less than the agency estimated last year, the recent CBO report added.

In the Biden administration's eyes, its efforts to raise taxes on the wealthy and big corporations, as well as recoup billions through IRS audits on the rich, will help boost revenue to fund key programs. Stronger GDP growth is also helping to whittle the deficit, they say.

Republican lawmakers, the Biden officials argue, could make the nation's debt and interest payment situation worse by extending Trump-era tax cuts that would add $3.5 trillion to the deficit through 2033. Currently, many of the provisions in the 2017 Tax Cuts and Jobs Act, which largely benefited wealthier Americans and corporations, will expire at the end of 2025, although some GOP lawmakers want to renew the cuts.

As it is, the federal government over the next decade is projected to spend a total of $12.4 trillion on interest — the highest amount of interest in any historical 10-year period, according to the Peter G. Peterson Foundation, a think tank that's focused on reducing the federal debt. That's the equivalent of about $37,100 per person, it said.

In 2023, the U.S. spent more on interest than on Medicaid, the health care program for low-income Americans, the foundation added. It is urging lawmakers to create a bipartisan fiscal commission that would create plans for lowering debt, among other issues.

How the Fed figures into all this

Experts say the nation's growing debt and interest payments could play a role in the 2024 presidential election. Republicans have sought to blame the Biden administration for excessive pandemic spending that they contend caused drover up inflation. Economists blame the surge in price on a range of factors, including supply-chain snarls, labor shortages, geopolitical factors such as Russia's war on Ukraine, and spending programs under both the Trump and Biden administrations.

The resulting interest-rate hikes by the Fed have been painful for families and small businesses, while also adding to the nation's interest burden, Republican members of the House Ways & Means Committee argue. "Rising interest rates, and the associated cost of servicing federal debt, are a direct result of President Biden and Democrats' inflationary spending spree," the GOP lawmakers said in a December statement.

Like American consumers, the U.S. could see some relief when the Fed begins cutting rates, which it is expected to do later this year. But the nation could still be trapped in a cycle of escalating interest payments as the U.S. is on track to take on more debt, Goldwein warned.

"More debt leads to more interest, and that leads to more debt," he said.

The CBO estimates that debt and interest payments will continue to grow over the next 10 years, with federal spending expected to jump 64% to $10 trillion, compared with $6.1 trillion in 2023. Much of that increase is due to mandatory spending programs, including Social Security and Medicare, whose costs are surging due to the aging U.S. population.

In Goldwein's view, tackling the nation's growing debt pile will require lawmakers on both sides of the aisle to focus on both raising revenue through higher taxes and cutting spending.

"It's not realistic to deal with it on only one side," he said.